Understanding Mutual Funds Ireland Basics

Picture an Irish mutual fund as a community baking project. Each investor brings ingredients—capital—and the fund manager whips up a diversified portfolio. By pooling money, you spread fees and risks across a wider mix of stocks, bonds or alternative assets.

In this section you will:

- See how €6.7 trillion in assets under management cements Ireland’s fund hub status

- Meet the watchdogs keeping the industry on the straight and narrow

- Compare the two flagship regimes, UCITS and AIF

- Digest core ideas with a simple concept map

'Ireland’s funds hub status relies on robust rules and a tax-efficient environment.'

Since the first UCITS fund launched in the 1980s, Ireland has grown into a full-service ecosystem. Today, 130 fund administrators and 30 depositaries handle thousands of vehicles.

The Central Bank of Ireland (centralbank.ie) enforces the rulebook, oversees reporting and champions transparency. Most funds opt for UCITS’ retail-friendly safeguards, while the AIF framework caters to professional investors. Splitting these regimes lets you pick the model that aligns with your goals and risk appetite.

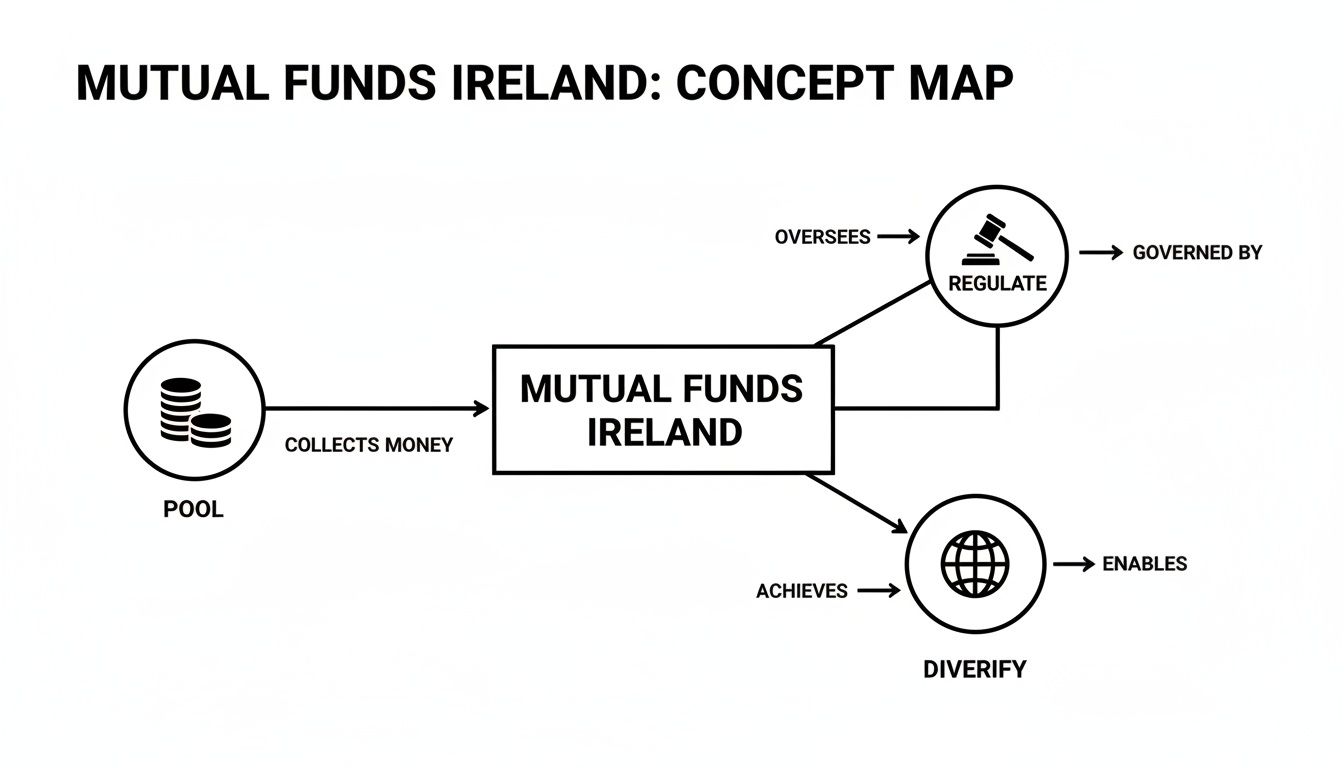

Key Concepts Visualised

Below is a snapshot of the fund lifecycle—pooling capital, applying regulation and diversifying risk across the globe.

Comparing UCITS And AIF

Ireland’s two main fund regimes serve different investor profiles under distinct rulesets. The table that follows breaks down their scope, who can join and how tax treatment varies.

UCITS Versus AIF At A Glance

| Feature | UCITS | AIF |

|---|---|---|

| Regulatory Scope | Harmonised EU rules designed for retail investors | Flexible EU framework for professional and institutional vehicles |

| Investor Eligibility | Open to all retail investors, with clear safeguards | Restricted to qualified or professional investors |

| Tax Treatment | Transparent structure with treaty benefits | Varies by fund type, potentially subject to withholding |

This snapshot should help you decide quickly which regime matches your investment strategy. Once you’ve got that sorted, the deeper dive into regulations and fund selection will feel a lot more straightforward.

Irish Mutual Fund Regulation And Taxation

Picture Ireland’s Central Bank as the conductor of a financial symphony, ensuring UCITS and AIF funds play in perfect harmony. It sets the tempo for oversight, sharpens risk controls and makes sure investors stay protected.

Behind the scenes, two major consultations—CP161 and CP162—have fine-tuned the rulebook, giving fund managers clear guidance on what’s expected and how to keep liquidity in check.

UCITS And AIF Rule Updates

By late 2024, CP161 refreshed UCITS guidelines with tougher liquidity management and extra guardrails for investors. A few months later, in Q3 2025, CP162 tackled AIFs head on—modernising private markets procedures and smoothing out co-investment restrictions.

- Liquidity frameworks got a serious upgrade

- Co-investment limits were clarified and made more flexible

- Upcoming SFDR consultations aim to boost operational resilience and ESG disclosures

Investor Classifications

Not everyone gets the same seat in this orchestra. The Central Bank splits investors into three groups:

- Retail Investors: Standard protections, redemption caps and clear risk warnings

- Professional Investors: Must meet asset or experience thresholds to qualify

- Sophisticated Investors: Gain access to bespoke AIF strategies and exclusive fund lines

Each tier carries different disclosure requirements and eligibility rules, so you know exactly which playbook applies to you.

SFDR Sustainability Requirements

For anyone tracking ESG, SFDR adds another layer on top of UCITS and AIF standards. Funds must pick their sustainability class and stick to it:

- Article 6: Standard funds reporting principal adverse impacts

- Article 8: Funds promoting environmental or social characteristics

- Article 9: Dedicated sustainability-objective funds

Managers need to publish both sustainability statements and pre-contractual disclosures—adding a few compliance steps but delivering greater transparency.

Tax Exemptions And Double Treaty Relief

A major perk for Irish-domiciled funds is generous withholding-tax relief, which cuts drag on returns. On top of that, stamp-duty relief on share transactions keeps secondary trading costs low.

For example, a U.S. investor in an Irish equity fund might see withholding tax cut from 15 % to 0 %, significantly boosting net yield. Key treaties with the United States, United Kingdom, Germany and France let investors claim relief right at the source. Savvy use of these treaties can meaningfully improve after-tax performance.

Ireland’s mutual funds ecosystem also benefits from state-backed vehicles. The Ireland Strategic Investment Fund (ISIF), celebrating its 10-year anniversary in 2025, has delivered €2.9 billion in gains since inception, with an annualised return of 3.4 %. It’s committed €8.8 billion across 248 investments, generating €21.4 billion in economic activity.

Meanwhile, the Future Ireland Funds launched in July 2024 with €10.5 billion, climbed to €13.5 billion today and are on track to exceed €16 billion by end-2025. Discover more insights about ISIF’s performance

Check out our guide on the Big Four Accounting Firms for insights into audit and depositary roles in fund compliance: Learn more about Big Four accounting practices

Stamp Duty Relief Details

Under Section 129A of the Stamp Duties Consolidation Act, Irish law waives stamp duty on fund share transfers. It’s a small detail but one that keeps trading fluid and costs near zero.

Keep an eye on Central Bank consultations so you can stay ahead of rule changes and ensure your funds remain in tune with the latest compliance requirements.

The Central Bank’s rulebook updates ensure resilience and sustainability across Ireland’s mutual fund industry.

Invest In Irish Mutual Funds

Ready to dive into mutual funds Ireland? Think of this as a guided walk rather than a maze. You’ll learn exactly where to open your account, how to fund it and what to watch out for before you hit “confirm”.

Compare Investment Platforms

- DEGIRO for low-cost trades: €2.50 per equity trade and sharp currency-conversion rates.

- Interactive Brokers for advanced tools: tiered pricing and access to global exchanges.

- Local Irish wealth managers for personalised advice: tailor-made portfolios with dedicated support.

- Robo-advisers for hands-off investing: pre-built portfolios and automatic rebalancing.

- Traditional banks for peace of mind: integrated banking and investing under one roof.

- Specialist fund platforms for direct access: zero intermediary spreads and clear, upfront fees.

Example Account Opening Steps

- Sign up with your email and personal details.

- Upload a passport or driving licence to verify your identity.

- Link a bank account in EUR, GBP or USD to fund your new wallet.

Most brokers wrap this up in under 24 hours.

This view highlights DEGIRO’s clean dashboard, low fees and simple currency options.

Navigate KYC And Funding

Before investing, you’ll complete Know Your Customer checks. You’ll need to upload proof of identity and a recent address document. This can take a few hours or sometimes a couple of days.

After approval, you’ll hit the minimums. Some platforms let you start with €100, while others—like bespoke wealth managers—might ask for €10 000. Fees scale with service level, so balance cost against hands-on support.

Funding your account in EUR, USD or GBP is usually straightforward. Many brokers let you hold multiple currencies, cutting out nasty conversion surprises.

Manage Costs And Liquidity

- Review platform fees every quarter to avoid unexpected charges.

- Check fund liquidity schedules so you know when you can cash out.

- Use limit orders to lock in your ideal entry price during volatile sessions.

- Hold currencies that match your fund’s base to dodge extra FX costs.

- Compare ongoing fund charges (TERs) across providers.

- Watch out for inactivity fees on accounts you’re not using.

| Tip | Benefit |

|---|---|

| Use limit orders | Control purchase price |

| Multi-currency accounts | Reduced exchange charges |

'Keeping fees low and understanding liquidity windows can make a real difference to your long-term returns.'

Place Your First Trade

With your account funded and KYC done, it’s go-time. Search for your fund’s ISIN, set your trade size and double-check every charge before you click.

- Scan the bid-ask spread to ensure fair pricing.

- Confirm the trading currency to avoid FX mismatches.

- Note the minimum redemption amount for your exit strategy.

Follow these steps, and what once felt tricky will become second nature.

Seek Ongoing Support

Choose a platform with reliable customer service—phone, email and live chat. Lean on these channels if you need help reviewing order confirmations or untangling any hiccups.

Next up, we’ll dig into how to select the right fund based on goals, performance and risk. By then, you’ll feel like a seasoned insider navigating Ireland’s mutual fund scene with confidence.

Choose The Right Irish Mutual Funds

Walking into a cake shop, you’re tempted by dozens of slices—each with its own flavour and price tag. Choosing an Irish mutual fund works much the same way.

First, pin down your goals: are you chasing growth, living off income, or striking a balance between both?

Next, think about how much risk you’re comfortable with and your time horizon. These decisions shape:

- Investment Objective: the fund’s main target and its tolerance for risk

- Asset Allocation: the blend of equities, bonds and cash, and where they’re located

- Historical Performance: a look back at returns and steadiness

- Risk Metrics: measures like volatility and maximum drawdown to gauge potential dips

- Fee Structure: what you pay up front, on exit and annually via the expense ratio

Evaluating Fund Performance

Historical returns give you clues on how the fund might behave in different markets. Compare 3, 5 and 10-year returns to spot consistent winners versus one-hit wonders. At the same time, track volatility—because a choppy ride could mean sleepless nights.

'A fund with lower volatility can smooth the ride and protect capital during swings.'

- Does it beat its benchmark year after year?

- Are its returns closely tied to market highs and lows?

- Have any drawdowns stayed under 15 %?

Analysing Fees And Costs

A tiny fee difference today can balloon into thousands lost down the road. Remember, funds often charge:

- An initial fee from 0.5 % up to 5 %, cutting into your starting capital

- A redemption fee (usually under 1 %) as a deterrent against quick exits

- An ongoing TER that ranges from 0.1 % for passive options to 1.2 % for niche strategies

Imagine a 0.2 % TER gap on €100 000 growing into a €20 000 difference over 20 years. A simple comparison table or scorecard can make these costs crystal clear.

Below is a snapshot from Morningstar showing fund ratings and performance metrics.

Here you’ll notice top funds carry a 4-star rating and an average 5-year return of 8.2 %, underlining how consistency often pays off.

Incorporating ESG Ratings

Under SFDR, every fund falls under an Article label:

- Article 8 funds highlight environmental or social factors

- Article 9 funds aim for clear sustainability outcomes

Weigh ESG scores in your analysis, especially if you want investments that align with your principles or regulatory needs.

- Check the fund’s carbon footprint and voting history

- Hunt for third-party ESG certifications and detailed reports

- Watch out for any controversies or excluded holdings

Learn more about expert advice on business valuation to see how fund pricing models resemble company appraisals.

Building Your Personal Scorecard

A scorecard turns gut calls into data-driven decisions.

- List your contenders and note down objectives, returns, fees and ESG ratings

- Rate each category from 1 to 5 based on your priorities

- Sum up the scores to rank funds and highlight your favourites

- Revisit the scorecard each year to capture shifts in markets or goals

Adjust the weight you assign to each factor as your strategy evolves. This process keeps you grounded and your portfolio aligned with what really matters.

Explore Market Size And Top Fund Managers

Ireland’s funds industry isn’t just big—it’s the beating heart of Europe’s mutual fund scene. By October 2025, Irish-domiciled vehicles commanded €6.7 trillion in assets under management. Roughly 65 per cent of that flows through UCITS, while the remaining 35 per cent sits in AIFs.

Key Market Metrics

- €6.7 trillion total AUM across UCITS and AIFs

- 78 per cent share of European ETF assets, roughly €1.8 trillion

- 96 per cent of Europe’s active ETF assets domiciled in Ireland

Industry Scale And Dominance

Think of Ireland as the engine room powering Europe’s ETFs. Irish funds hold a 78 per cent stake of all European ETF assets, amounting to €1.8 trillion by late 2025. Even within active ETFs, Ireland claims a staggering 96 per cent slice—about €85.5 billion.

- 94 per cent of year-to-date net ETF inflows in 2025, equivalent to $41.5 billion

- Over 150 authorised fund firms managing nearly 14 000 vehicles

220 of 260 active ETF structures and 429 of 496 share classes domiciled in Ireland—proof of the market’s intense focus.

For a deeper dive, check out the Irish Funds Industry Statistics.

Top Fund Managers Comparison

Below is a comparison of leading managers by Irish-domiciled AUM, European ETF share and speciality.

Top Five Fund Managers In Ireland

| Manager | AUM (€ bn) | European ETF Share (%) |

|---|---|---|

| BlackRock | 850 | 30 |

| Vanguard | 420 | 15 |

| State Street | 300 | 12 |

| JP Morgan Asset Management | 250 | 8 |

| Amundi | 200 | 5 |

Together, these five giants control over 60 per cent of AUM, shaping everything from passive ETFs to active strategies.

Key Takeaways

- Ireland’s deep liquidity and prudent regulation cement its fund hub status

- ETFs remain the primary growth engine, with active ETF inflows outpacing rivals

- Global managers favour Ireland for smooth EU access and operational efficiency

- The UCITS framework safeguards retail investors, while AIFs fuel institutional innovation

For anyone investing in Irish-domiciled funds, these figures spotlight where to focus. Keep an eye on evolving Central Bank consultations and EU directives to stay ahead.

Central Bank Tracking

The Central Bank of Ireland regularly publishes detailed figures on fund positions, transactions and exposures. Those numbers feed into national accounts and shadow banking metrics, offering full transparency for investors and policymakers.

As of October 2025, the Central Bank reported growth across both UCITS and QIAIF assets, underscoring Ireland’s ongoing appeal.

Despite high concentration, newcomers carve out niches in ESG, private credit and thematic ETFs—keeping the market lively.

Future Trends In Fund Management

Looking ahead, expect sustainable and tech-focused funds to gather steam. Digital asset integration and smoother cross-border distribution will define the next chapter.

- Greater SFDR alignment driving a new wave of ESG fund launches

- Expansion of private markets strategies within QIAIF structures

- Enhanced investor reporting via digital portals and real-time data

Arming yourself with today’s market size, top players and regulatory framework sets you up for success—whether you’re launching a fund or building a portfolio. Ireland’s track record explains why global asset managers keep making it their home.

Next, we’ll dive into practical tips for investors and fund founders.

Practical Tips For Investors And Founders

Navigating Irish mutual funds isn’t a freefall—it’s more like exploring a mapped trail. A solid set of pointers becomes your field manual for everything from compliance checks to performance tracking.

Keep investor tasks and founder duties in separate lanes. That way, you stay nimble on both fronts and adapt quickly to market twists.

Effective Due Diligence Practices

Before writing a cheque, dive deep into the numbers and paperwork. Start by reviewing the Fund Prospectus, Key Investor Information Document (KIID) and offering documents.

Then, set up quarterly reminders for updates and full audit reports. Catching tweaks in regulations or shifts in strategy early is a game-changer.

- Compare fund objectives to current market themes.

- Verify Compliance Certificates from the Central Bank of Ireland.

- Track portfolio turnover rates to see how often managers trade.

- Confirm credentials of administrators and depositaries.

Efficient Portfolio Management

Think of your holdings as a garden: it needs scheduled pruning and watering. Regular rebalancing smooths out the bumps when one asset class outgrows the others.

Rebalance every six months or whenever an allocation drifts more than 5 % from your target. That discipline keeps your risk in check and your returns on track.

- Measure current weights against your ideal mix.

- Buy or sell to restore balance—focus on currency and sector exposures.

- Log transaction costs carefully to avoid surprises.

'Consistent rebalancing removes emotion and keeps performance on track.'

Screenshot From Regulatory Source

Below is a screenshot from the Central Bank’s website showing recent regulatory updates impacting Irish funds.

This visual highlights updated reporting deadlines and enhanced liquidity requirements, emphasising the need for timely compliance.

Tips For Fund Founders

Building share classes is more art than rush job. Separate structures for retail, institutional or performance-fee investors bring clarity and keep regulators happy.

Key reminders:

- Draft concise disclosure documents that spotlight fee differences.

- Pick depositaries well-versed in Irish fund rules.

- Choose administrators with robust digital reporting tools.

- Align every service provider to your fund’s long-term plan.

You might be interested in our guide on funding options for acquisitions. Check out our guide on four ways to fund a business acquisition to see how different capital strategies can support fund launches.

Ongoing Monitoring And Adaptation

Funds that thrive today embrace change tomorrow. Build a dashboard to track:

- Net Asset Value (NAV) movements

- Compliance incidents or exceptions

- Expense Ratio trends

- Investor inflows and outflows

Review the dashboard every month. A sudden spike in redemptions could flag liquidity stress or a shift in sentiment.

Best Practices To Avoid Pitfalls

- Keep a centralised document library with strict version control.

- Automate alerts for regulatory filings and client communications.

- Schedule an annual independent compliance review.

- Monitor tax treaty changes to preserve efficiency.

Regular checkups reduce surprises and build investor trust.

Annual Strategy Reviews

Once a year, gather key stakeholders for an Annual Strategy Meeting. Revisit your fund’s goals, scan market trends and consider swapping service providers if needed.

- Time the review after major Central Bank announcements.

- Challenge assumptions and refresh your playbook.

By embracing these battle-tested tips, both investors and founders can move confidently through Ireland’s rigorous mutual funds environment. Habitual due diligence, smart portfolio moves and transparent fund structuring will help you sidestep common errors and boost long-term returns. Stay curious, stay proactive—and the numbers will follow.

Frequently Asked Questions

Q1 What Are the Main Types Of Irish-Domiciled Funds?

Many investors find themselves asking which fund structure is the best fit. In Ireland, you’ll typically encounter UCITS, QIAIFs and MMFs—each with its own rulebook and purpose.

- UCITS: Designed for retail investors. You get daily pricing plus harmonised EU regulation.

- QIAIFs: Geared towards professional clients. These funds offer more flexibility and higher risk limits.

- MMFs: Short-term vehicles focused on cash preservation and stable net asset values.

'Choosing between UCITS, QIAIFs and MMFs lets you balance regulation and flexibility to suit your objectives.'

Tax Treaty Relief

A good tax treaty can mean more money in your pocket. By tapping into withholding tax relief and double-taxation agreements, you can meaningfully boost your net distributions.

- Withholding tax relief under Irish treaties may reduce dividend deductions to 0 %, depending on your home country.

- Double-taxation agreements let you claim credits on overseas withholding at source.

- Filing timely treaty claims can add 2–3 % net yield on distributions.

Just remember to submit the relevant treaty claim forms through your fund platform before distribution dates.

Q3 What Minimum Sums Do I Need To Invest?

Entry thresholds vary by platform and fund type. Here’s a quick snapshot:

| Platform | Minimum (€) |

|---|---|

| Online brokers | 100 |

| Wealth managers | 10 000 |

| Specialist platforms | 1 000 |

'Many retail investors start from €100, making Irish funds very accessible.'

Some bespoke managers may set higher minimums in return for premium services. Compare fees and thresholds side by side to find your sweet spot.

Sustainable Fund Labels

SFDR labels give you a roadmap for sustainable investing. Understanding Articles 6, 8 and 9 ensures your portfolio reflects your values.

- Article 6 funds handle standard reporting of principal adverse impacts.

- Article 8 funds actively promote environmental or social characteristics.

- Article 9 funds pursue defined sustainability objectives with robust disclosures.

'SFDR labels bring clarity and help target fund choices to your sustainability goals.'

Always review the Key Investor Information Document to verify a fund’s classification and features.

Actionable Tips For Investors

- Match UCITS, QIAIFs or MMFs to your risk profile.

- Confirm withholding tax relief rates before you invest.

- Start small with €100 or opt for higher-service platforms if you need extra support.

- Use SFDR labels to align your investments with your environmental and social goals.

Keep this FAQ handy as you explore Irish mutual funds and invest with confidence.

Discover more from Scott Dylan

Subscribe to get the latest posts sent to your email.